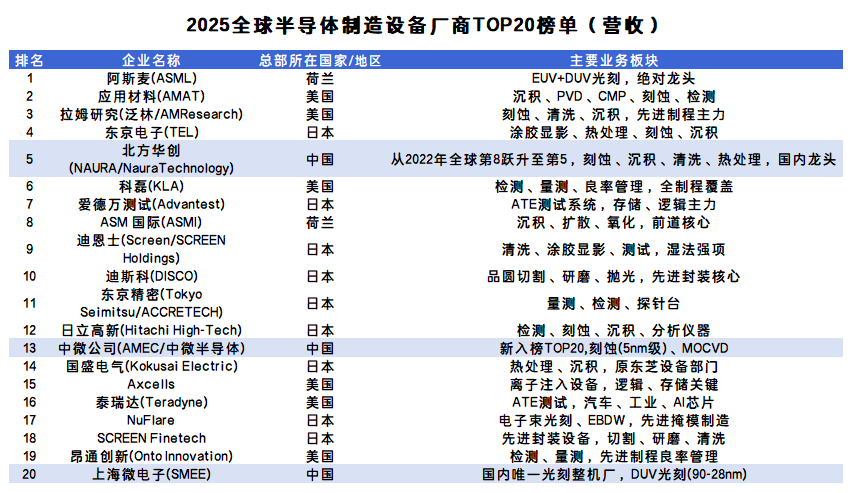

According to the 2025 Global Top 20 Semiconductor Equipment Manufacturers ranking recently released by the Japanese research institute Global Net, Asian companies account for more than half of the companies on the list. Among them, nine are Japanese and three are Chinese, highlighting Asia’s expanding presence in the upstream segment of the global semiconductor equipment industry.

From a breakdown by country, Japanese firms lead in number and continue to demonstrate long-term technological accumulation and market share advantages across key segments including etching, deposition and inspection equipment.

On the Chinese side, three companies made the Top 20. NAURA Technology Group Co., Ltd. rose to fifth place globally, up three positions from 2022. The company focuses on the research, development and manufacturing of core semiconductor process equipment, including etching systems, physical vapor deposition (PVD) and chemical vapor deposition (CVD) tools.

In addition, Advanced Micro-Fabrication Equipment Inc. China (AMEC) and Shanghai Micro Electronics Equipment (Group) Co., Ltd. (SMEE) entered the ranking for the first time. AMEC specializes in plasma etching and chemical thin-film deposition equipment, with products applied in micrometer- and nanometer-scale device manufacturing. SMEE’s business scope covers semiconductor equipment, pan-semiconductor equipment and high-end intelligent manufacturing equipment.

From a market perspective, amid a rebound in global chip prices and improving demand for certain memory products, the semiconductor equipment sector has attracted renewed investor attention, with related ETFs and individual stocks posting recent gains. Institutional analysts note that under the combined impact of pricing and demand shifts, the operating performance of memory and equipment companies warrants continued observation. Market focus is expected to center on product price trends and the sustainability of corporate earnings.

More broadly, several technology companies have disclosed recent operational and strategic updates. Huawei Technologies Co., Ltd. Chairman Liang Hua stated publicly that the company’s 2025 sales revenue exceeded RMB 880 billion, emphasizing continued focus on core businesses and high-quality development.

In international markets, Panasonic Holdings Corporation announced that starting in April 2026 it will transfer its television sales business in Europe and North America to Skyworth Group Limited. The two sides plan to cooperate in sales, research and development, and manufacturing.

In the fields of cloud computing and artificial intelligence, data center projects advanced by Oracle Corporation, OpenAI and SoftBank Group Corp. have drawn market attention, with certain adjustments made to computing capacity deployment plans.

Regarding supply chain arrangements, Apple Inc. stated that part of the production process for Mac mini will be relocated to the United States, to be undertaken by local facilities of Hon Hai Precision Industry Co., Ltd. (Foxconn).

Overall, semiconductor equipment sits at the very upstream of the semiconductor industry and serves as a foundational pillar of chip manufacturing. Its technological capability and supply stability are closely monitored by stakeholders across the value chain. The fact that Asian companies account for more than half of the Top 20 reflects the region’s progress in research and development, manufacturing capacity and market expansion. Future industry trends will continue to be shaped by global demand dynamics, technological evolution and industrial policies across major economies.