(Asian Observer reporter Kelly, Tokyo, December 11)

Prologue | What Is Happening to the World?

This year, the world has never been short of news.

Markets fluctuate daily, policies are rolled out one after another, technologies advance at breakneck speed, and the flow of capital and data seems endless.

Yet amid this constant noise, one fundamental question has grown clearer, sharper, and more urgent—

What, exactly, is happening to the world?

Why has money never been more abundant, while the sense of personal wealth feels increasingly scarce?

Why do macro tools keep appearing, yet micro-level anxiety refuses to recede?

Why do technological frontiers expand rapidly, while our sense of security subtly retreats?

Why are market narratives as lively as ever, while the real stories of the economy are harder and harder to tell?

These questions transcend borders and cut across social strata.

They echo simultaneously in Europe and the United States, across Asia, Africa, and Latin America; they manifest in nations large and small, and are embedded in corporate balance sheets, household decisions, and individual life planning.

This is not the shock of a single event, but the impact of a moment when many “once-taken-for-granted rules” appear to be failing at the same time—producing a widespread and visceral sense of dislocation.

This is why we launch this year-end observation.

Not to offer a simple answer, but to return to the concrete realities on the ground—

to the profit-and-loss lines of businesses, the consumption lists of families, the testing grounds of policy, the hesitation points of the market, and the Z generation oscillating between “hyper-competition” and “lying flat.”

By linking signals that seem isolated on the surface, we seek to uncover the deeper connections behind them.

If the world is indeed facing a certain predicament, perhaps it is not because it has suddenly deteriorated.

Rather, it may be because we are still holding an old “blueprint” while trying to measure an era whose underlying logic has already been reshaped.

This is what we aim to document and present—

a deep inquiry into the world we live in today.

What is happening to the world?

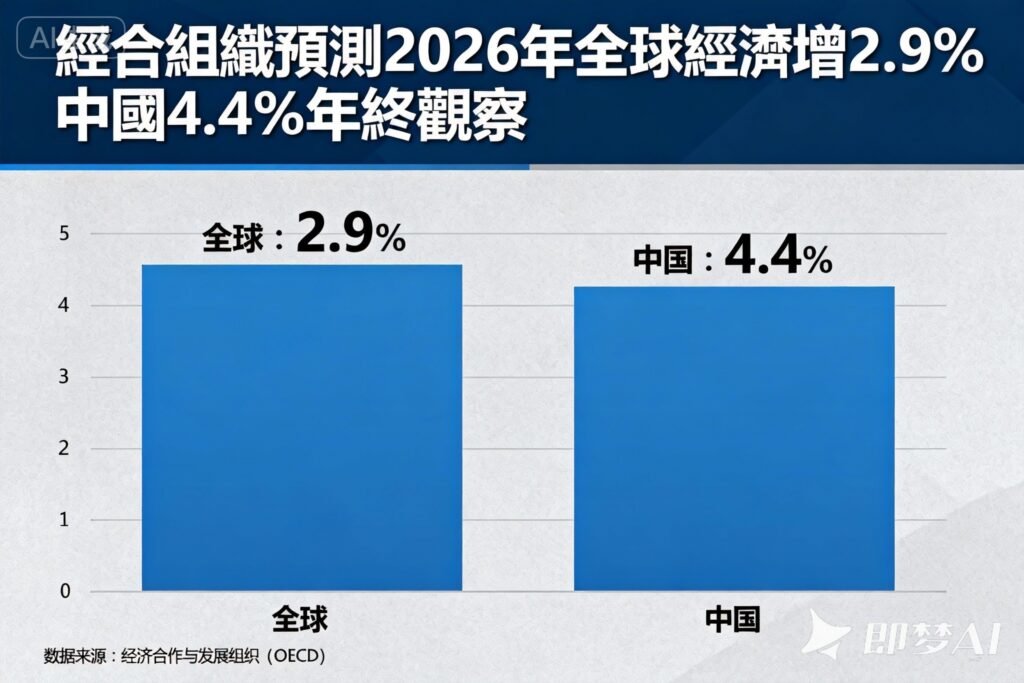

As 2025 draws to a close, the Organisation for Economic Co-operation and Development (OECD) has released its latest Economic Outlook report, providing an annual “health check” of the global economy and its forecasts. The report shows the global growth outlook for 2025 has been revised slightly upward to 3.2 percent, but growth is expected to slow to 2.9 percent in 2026.

According to the OECD, China’s growth forecast has been revised upward, with 2025 expected to grow 5 percent, above the September estimate of 4.9 percent, while growth in 2026 is projected to slow to 4.4 percent.

Growth slowing, resilience intact

Based on the OECD’s December forecast, the global economy is expected to show strong resilience in 2025 before slowing modestly in 2026.

Global GDP growth is forecast to fall from 3.2 percent in 2025 to 2.9 percent in 2026, then recover slightly to 3.1 percent in 2027.

This moderation is not unexpected. As early as March 2025, the OECD warned in an interim report that global GDP growth would slow moderately due to rising trade-policy uncertainty and heightened geopolitical tensions.

Short-term strength and medium-term pressure

Among major economies, China’s growth outlook stands out. The OECD raised China’s 2025 forecast from 4.9 percent in September to 5 percent, while keeping the 2026 projection unchanged at 4.4 percent.

This revision reflects China’s combination of short-term resilience and medium-term challenges.

According to the report, the main reasons for China’s slower growth in 2026 include reduced fiscal support and the impact of new U.S. tariffs on Chinese imports.

U.S. economy expected to grow 2 percent in 2025

The global economic landscape shows a divergent pattern of growth. Compared with September forecasts, the OECD revised up the short-term outlook for the United States, Eurozone and Japan.

The U.S. economy is now expected to grow 2 percent in 2025, up from the earlier forecast of 1.8 percent. Growth in 2026 is projected at 1.7 percent, also above the previous estimate of 1.5 percent. The Eurozone, supported by a strong labor market and increased public spending in Germany, saw its 2025 forecast raised from 1.2 to 1.3 percent.

Japan’s outlook has also improved, with 2025 growth now expected at 1.3 percent, compared with the previous 1.1 percent.

AI investment boom provides lift

Despite multiple risks, the global economy continues to display resilience, supported by structural factors.

The OECD notes that the investment boom in artificial intelligence is helping offset some of the negative impact of U.S. tariff hikes and has become a key pillar supporting global growth. AI investment, fiscal support and expectations of U.S. Federal Reserve rate cuts are jointly helping counteract the drag from import tariffs, declining immigration and federal workforce reductions.

This indicates that technological innovation is increasingly acting as a stabilizing force in the global economy.

Trade tensions and policy uncertainty

Despite the supportive factors, the OECD warns that global growth remains highly vulnerable to any new escalation in trade tensions. It cautions that if investor optimism toward AI proves overly optimistic and fails to deliver, stock markets may face corrections.

The full impact of tariffs on investment and consumption has already become evident. Global trade growth is forecast to slow from 4.2 percent in 2025 to 2.3 percent in 2026, as rising trade-policy uncertainty constrains recovery prospects.

The OECD’s March report also warned that global growth remains exposed to renewed trade tensions.

Policy choices determine trajectory for 2026

In this complex environment, policymakers’ decisions will play a decisive role in shaping future growth pathways. The OECD urges countries to strengthen cooperation within the global trading system and work toward making trade policies more predictable.

It stresses that agreements easing trade tensions and reducing existing trade barriers, along with clear and transparent trade policies, will enhance policy certainty and improve the investment and growth outlook.

Central banks should maintain vigilance, continuing interest-rate cuts when inflation is stable at or moving toward target levels, while remaining ready to adjust policy if inflation pressures resurface or labor markets weaken unexpectedly.

As the year-end approaches, the International Monetary Fund (IMF) has also revised its global growth forecast. Despite trade tensions and geopolitical uncertainty, the IMF lifted its 2025 global growth forecast slightly to 3 percent. The Director-General of the World Trade Organization recently called for the United States and China to ease trade tensions, warning that a “decoupling” between the two major economies could lower global output by 7 percent in the long term.

The global growth trajectory in 2026 will be shaped by a balance between the innovative momentum of AI and the headwinds created by trade frictions.