Hong Kong Permits Tokenised Fund Trading, Allows Night and Weekend Trading

The Hong Kong Securities and Futures Commission (SFC) announced a new regulatory framework on the 20th, promoting secondary market trading of SFC-authorised tokenised investment products (tokenised products) in Hong Kong on a pilot basis, in order to support the further development of the digital asset ecosystem. It also issued clear guidance on areas such as “trading channels”, “fair pricing” and “liquidity provision”. Julia Leung, CEO of the SFC, stated that the new framework is innovative and scalable, providing robust investor protection, and allowing traditional securities products to be traded at night and on weekends after tokenisation. The first batch of products is expected to be mainly tokenised money market funds, and the SFC will consider expanding the product scope in due course.

Since the SFC first defined the tokenisation regulatory framework at the end of 2023, product issuers in Hong Kong have been actively promoting product tokenisation. As of March this year, 13 tokenised products have been offered to the public in Hong Kong, and the total assets under management of their tokenised share classes have increased approximately sevenfold over the past year, reaching HK$10.7 billion. Therefore, the SFC decided to promote 24/7 secondary market trading, hoping to further integrate tokenised products with the Web3 ecosystem through the application of regulated stablecoins and tokenised deposits in transactions.

Ms. Leung said the new framework marks another important milestone in Hong Kong’s development of a digital asset ecosystem – a comprehensive and integrated ecosystem that is innovative and scalable while providing robust investor protection. She pointed out that the new initiative allows traditional securities products to be traded at night and on weekends after tokenisation, and promotes round-the-clock liquidity through the use of regulated stablecoins and tokenised deposits, responding to investors’ needs in an increasingly rapid and uncertain market environment.

Howard Chan, Under Secretary for Financial Services and the Treasury of the Hong Kong SAR Government, said that the SAR government has always maintained an open and positive attitude towards Web3 development. Hong Kong will steadily advance the development of the digital asset industry, continue to uphold the principle of “same business, same risks, same rules”, and continuously optimise a regulatory system that suits local conditions while meeting international standards, ensuring a healthy, responsible and sustainable development of the digital asset market, further consolidating Hong Kong’s position as an international financial centre.

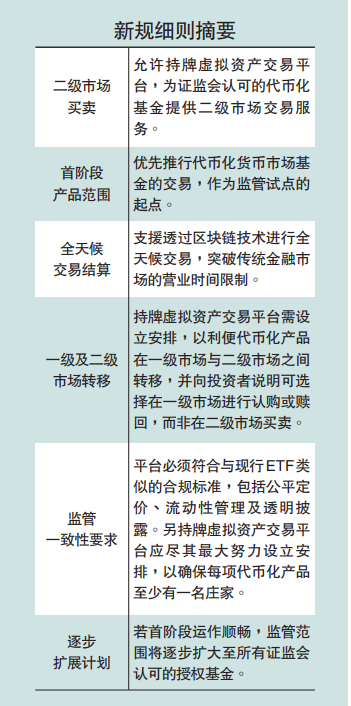

It is understood that the first batch of products for secondary market trading by the Hong Kong public will mainly be tokenised money market funds. The SFC will review the operation of these products and consider expanding the product scope in due course. The SFC’s circular provides the following guidance on “trading channels”, “fair pricing” and “liquidity provision”:

Trading with full funds – margin trading prohibited

Trading channels: Retail investors can conduct secondary market trading of tokenised products through SFC-licensed virtual asset trading platforms. Licensed platforms should only execute trades for clients when the client’s account holds “sufficient funds” or equivalent interchangeable product positions – meaning trading on margin is not allowed.

Fair pricing: Licensed platforms should implement effective risk management and monitoring measures, including issuing alerts to investors when the transaction price deviates significantly from the real-time or near-real-time indicative net asset value per unit. At the same time, platforms must explain to investors that they have the option to subscribe or redeem at net asset value in the primary market, and the associated implications.Liquidity provision: The SFC requires licensed platforms to ensure that each tokenised product has at least one market maker, and that any market maker must give at least three months’ prior notice before terminating its service. Platforms must closely monitor secondary market trading activities and liquidity of tokenised products, maintain close communication with appointed market makers, and formulate appropriate contingency plans. In addition, platforms must establish arrangements to facilitate the transfer of tokenised products between the primary and secondary markets. For example, tokens subscribed through the primary market can be conveniently traded in the secondary market, and tokens purchased in the secondary market can be redeemed through the primary market.

What is a tokenised fund?

A tokenised fund is essentially a traditional investment fund, such as a mutual fund or money market fund. The innovation lies in converting the fund’s “shares” into digital tokens on a blockchain, each token representing the investor’s partial ownership of the fund’s assets. Simply put, traditional beneficial certificates are turned into crypto-assets that can be circulated on the blockchain.Tokenised funds have two major advantages: high efficiency and low cost: traditional fund settlement takes days and incurs high fees; tokenisation uses smart contracts for instant settlement, almost instantaneously, greatly reducing costs. Low threshold and good liquidity: traditional private equity funds often require entry fees of millions of dollars and are difficult to cash out; tokenisation can split assets into tiny units, allowing small investors to participate, and enabling 24-hour trading and instant cash-out.